Motor fuel taxes are taxes levied on gasoline, diesel, and gasohol (a mixture of ethanol and unleaded gasoline). State and local governments collected a combined $53 billion in revenue from motor fuel taxes in 2021.

Most states levy per unit taxes based on how many gallons of gasoline a consumer purchases. However, 22 states and the District of Columbia tie at least a portion of their motor fuel tax rate to a variable such as the price of gasoline (wholesale or at the pump), inflation, or another metric (e.g., state population growth).

State and local governments collected a combined $53 billion in revenue from motor fuel taxes in 2021, or 1.3 percent of general revenue. (This total excludes any revenue collected from general sales taxes levied on motor fuel purchases in addition to the motor fuel tax.) Nearly all motor fuel tax revenue (97 percent) came from state motor fuel taxes in 2021.

States earmark most of their motor fuel tax revenue for transportation spending. In 2021, state and local motor fuel tax revenue accounted for 26 percent of highway and road spending. Toll facilities provided another 8 percent and the remaining 66 percent came from other revenue sources.

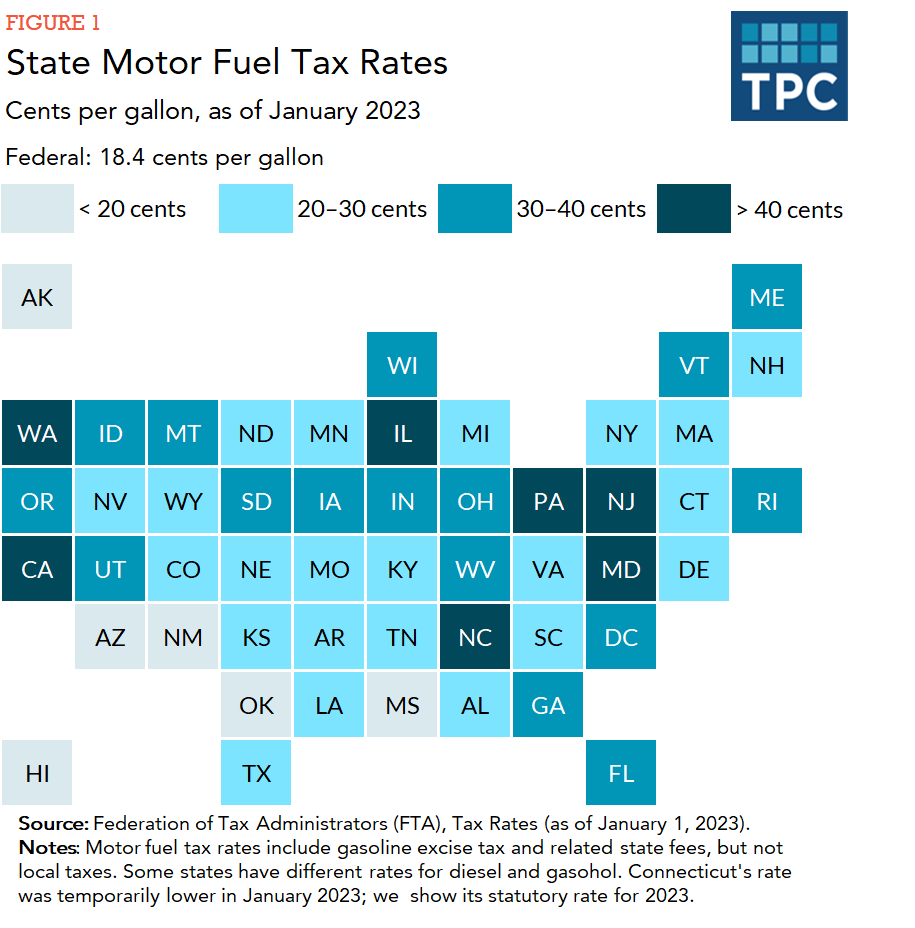

In addition to the 18.4 cents per gallon federal tax on motor fuels, all states and the District of Columbia tax motor fuels. Per gallon gas tax rates range from 8.95 cents in Alaska to 62.9 cents in California. In addition to Alaska, five other states have per gallon gas tax rates below 20 cents: Arizona, Hawaii, Mississippi, New Mexico, and Oklahoma. After California, the next-highest per gallon tax rates are in Pennsylvania (57.6 cents), Washington (49.4 cents), Illinois (43.4 cents), and Maryland (42.7 cents). These rates include any state excise taxes on gas plus any related taxes and fees that the consumer pays at the pump, such as applicable environmental or inspection fees.

Ten states also levy a general sales tax or gross receipts tax on purchases of motor fuel. In California, the (prepaid) general sales tax is included in the state’s per gallon excise tax rate. In the other nine states, the general sales tax or gross receipts tax is levied as a separate tax on the purchase.

State tax rates on gasohol are the same as tax rates on gas in every state except South Dakota, where the rates on gasohol are slightly lower. State tax rates on diesel fuel are the same as the tax rates on gas in 24 states and the District of Columbia, higher in 19 states, and lower in six states. For each state's tax rates on gas, diesel, and gasohol see our full table of state motor fuel tax rates.

Connecticut, Florida, Georgia, Maryland, and New York suspended their gas tax for a period of time in calendar year 2022. Additionally, Illinois and Kentucky stopped scheduled gas tax rate increases from taking effect. Policymakers pushed gas tax holidays in 2022 as the pandemic, the war in Ukraine, and various other factors increased the price of gasoline across the country.

In most states the gas tax is a per unit tax. That is, the consumer pays tax based on the number of gallons purchased rather than a percentage of the final purchase price. As a result, tax revenue increases only if drivers buy more gasoline or lawmakers raise the tax rate.

During the past two decades, Americans drove fewer miles and purchased more fuel-efficient vehicles. Consequently, aggregate gasoline consumption stagnated.

For most of this period, most states did not respond to a flat or declining tax base with tax rate hikes, and as a result inflation-adjusted state and local motor fuel tax revenue was higher in 2007 ($47.2 billion) than it was in 2014 ($46.8 billion). At the same time, construction costs and demands for transportation project spending continued to increase. Thus, many states faced transportation funding gaps.

As a result, in recent years, many states have made changes to their gas tax. Between 2013 to 2021, 33 states and the District of Columbia enacted legislation that increased their gas tax—but often in different ways.

In fact, states have various options when increasing transportation funding, including:

Tax miles traveled instead of gasoline. Oregon and Utah are currently running pilot programs that tax certain drivers' vehicle miles traveled (VMT) instead of gasoline purchased. The US Department of Transportation is also providing funding for additional VMT studies in several other states, and the Infrastructure Investment and Jobs Act created a national motor vehicle per-mile user fee pilot program. The hope is that a VMT tax can provide a more stable tax base as drivers increasingly purchase hybrid and electronic vehicles. However, there are administrative challenges with a VMT tax and governments would still need to set tax rates high enough to produce the desired amount of revenue.

Auxier, Richard C., and John Iselin. 2017. Infrastructure, the Gas Tax, and Municipal Bonds. Washington, DC: Urban-Brookings Tax Policy Center.

Boddupalli, Aravind, and Erin Huffer. 2020. What Do Federal Taxes Have To Do With Your Public Transit?. Washington, DC: Urban-Brookings Tax Policy Center.

Auxier, Richard C. 2017. Four Facts for Trump's Infrastructure Week. Washington, DC: Urban-Brookings Tax Policy Center.

Interactive Data Tools